Case Study 1 : Intuit Mint

Prompt: Scale Intuit’s Mint to a larger audience, build a product to increase engagement, and drive growth.

“Intuit is a global technology platform with a mission to power prosperity around the world” - Intuit

“Intuit's business model focuses on creating customer value through trusted, effective software.” - Intuit

Image 1: Intuit’s products & monthly active users(MAU’s)

Image source https://intuit.com/

Introduction & Product Background

Intuit is a leading provider of financial management software for consumers, small businesses, and accounting professionals. Their innovative products like TurboTax, QuickBooks, Credit Karma, Mint, and Mailchimp help millions of customers with accounting and bookkeeping.

Mint is a B2C SaaS personal finance product that helps users manage all their finances in one place. It’s a niche category of Personal Finance Management (PFM) that can be configured to categorize transactions and add accounts from multiple institutions, spending trends, and budgets into a single view to include data visualizations. Currently Mint has over 29M registered users but a mere 3.6 Monthly Active Users(MAUs) with just over 12% conversion rate with revenue predominately generated through ads and some premium subscriptions.

In this case study, I try to decipher how Mint can approach this obstacle to increase engagement while retaining its unique value proposition(UVP) of helping users solve their financial problems. Hypothesis and solutions are derived based on my own data collection through customer interviews within my network, polls, interviews, and current & future market trends. Since I do not have access to any of the internal data and consumer study reports, I’m relying on the data I’ve collected through personal means to make the best judgment possible.

Image 2: Intuit’s Strategy

Image source https://intuit.com/

2. Company Mission and Values, Roadmap, Products

Intuit’s vision for its products is “Overcome Your Financial Challenges” and it reflects in the ecosystem of products it develops geared mostly towards individuals and small businesses. Mint has had quite a run-up to find its Product Market Fit over the years, now more than ever Mint needs to find solutions to differentiate itself from the rest of its competitors to be the unanimous leader in the PFM market.

Image 3: Intuit’s marquee manifesto across all products

3. Market and Competitors Analysis

Direct competitors: YNAB, Acorns, Sofi, Simplifi

Indirect competitors: CPAs, Manual finance tracking with Excel sheets, Financial advisors

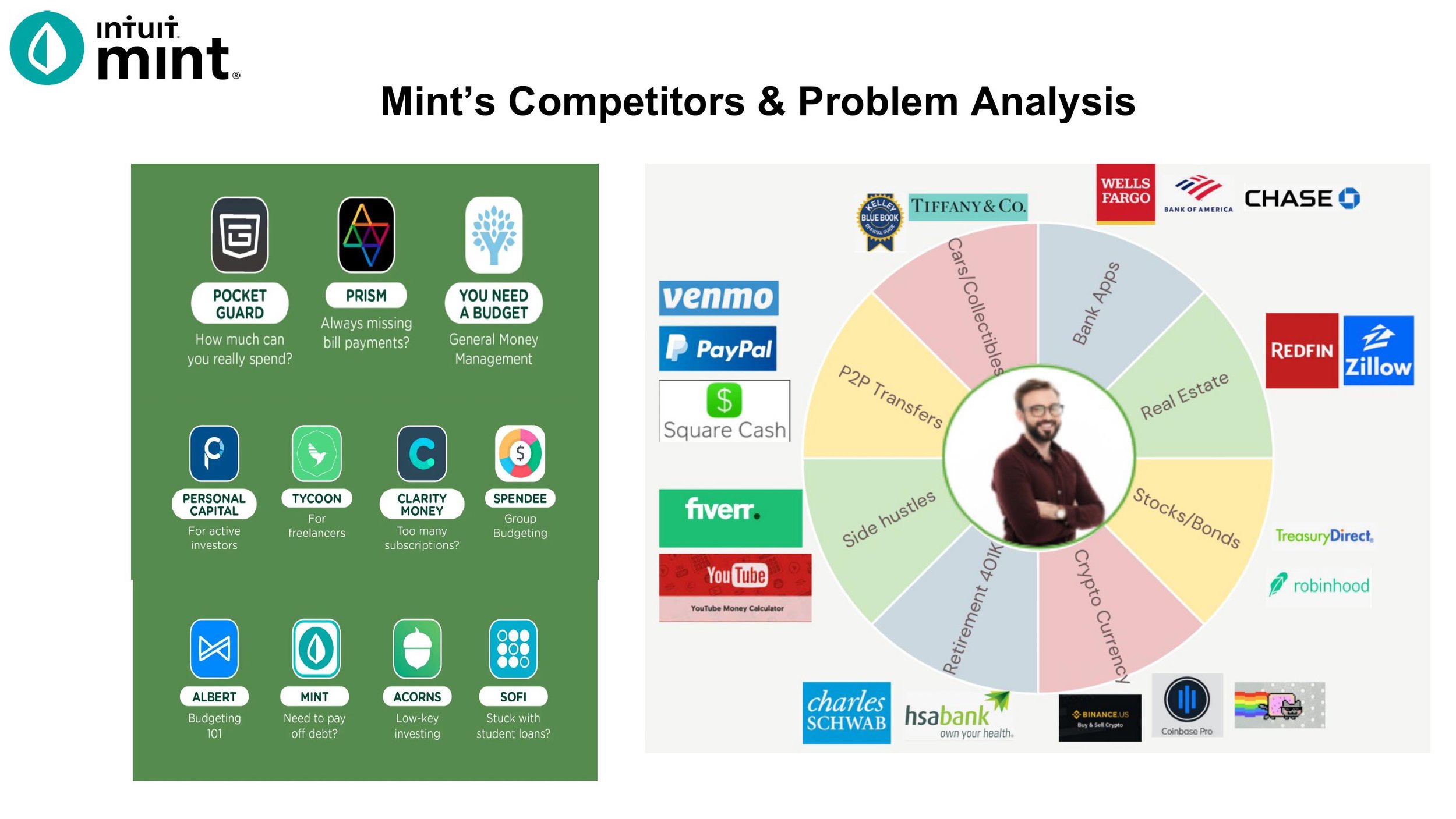

Image 4: Personal Finance Management(PFM) Apps & Mint’s competitors

Image 5: Porter’s Five Forces - Mint App market position evaluation

4. User Research and Personas

The process of collecting user data is the most critical one for defining a solution that lays the foundation for a future Product Market Fit. The wider the sources, the better data points but they don’t necessarily arrive at congruent conclusions. Knowingly or unknowingly, what people say they positively respond to, could be widely different from the ones they actually do in real life, so collecting both quantitate and qualitative metrics is essential to arrive at an optimized solution using UX research data-driven approach.

For the purposes of this case study, I’ve simplified the process. I interviewed a wide range of people who are current & former Mint subscribers and others who budget differently using supplemental resources and collated them to transform them into user personas.

Image 6: User Research Methods

Image 7: Mint - User Personas

5. Brainstorming Solutions

Coming up with product solutions starts absolutely with the customer pain points. While it’s tempting to solve every user problem from every segment possible, there’s always a tradeoff between risk vs rewards which dictates what features need to get built with a priority.

While short-term solutions and fixes have their place in the product cycle, they might not impact the customers immensely or bring everlasting gains to the organization. Hence, building toward solving a big enough problem with a bigger market opportunity by brainstorming moonshot ideas helps the final product land somewhere in the middle of reality, after discounting for unknown complexities/roadblocks ahead.

Image 8: Features prioritized using RICE Framework

6. Prioritization, Tradeoffs for ROI, and Success metrics/KPIs

Feature prioritization is done with abundant customer studies, surveys, internal & external data with quantitative ranking, and formulating matrices with values directly tied to the customer feedback which align with the organization’s mission and goals. Feature prioritization reduces the risk of building a product that burns resources, in addition to the opportunity costs of not building the product that the customer desired in the first place. Additionally, it improves the probability of a big return on investment (ROI).

There are plenty of product prioritization frameworks used to decide which product/feature to build, here are a top few:

a) The Kano Model: Mapped on a 2-dimensional plot with user satisfaction vs functionality, the highest delight and functionality is chosen.

b) The MoSCoW method: Must have, Should have, Could have and Wont have, the best solution bubbles up via feature eliminations.

c) RICE Framework: Reach, Impact, Confidence, and Effort. The feature with the highest formulated RICE score gets the pick.

d) ICE Scoring Model: Impact, Confidence, and Ease. The highest relative average ICE score features bubbles to the top.

e) Opportunity Scoring: Evaluates the feature importance, customer delight, and satisfaction.

f) Weighted Scoring Prioritization: Numerical scoring which ranks strategic initiatives against cost/benefit categories for prioritization

When features are chosen to prioritize with any of these frameworks, logically it makes sense put all the focus and resources to pick the highest scoring feature to build. But it might or might not be the best path to go after strategically. The reason is, that there are plenty more parameters to consider during a product cycle like resource interplay, tech debt, competitors’ pressure with time to market, complexity with the tech stack, engineering resource constraints, and blockages with any or all of those in conjunction.

To simplify this case study, I don’t have access to all the consumer studies and user research, but I have relied on the data collected, coupled with my intuition for what the future marketplace needs, keeping in mind Intuit’s global market positioning to arrive at an informed decision.

6.1 Short to mid-term product to build - AI/ML Net worth Estimator and Personalized Finance Bot:

My hypothesis for choosing the AI/ML Net worth Estimator Personalized Finance Bot is primarily rooted in customer empathy and the pain points it resolves with the value it delivers to the users.

Many of us go through our entire adult life with being financially illiterate or ignorant, and going through an economic downturn without the knowledge of wealth creation or management can be daunting to some individuals and it doesn’t have to remain that way for long. This situation is what Intuit can leverage, to build a product that helps users lower the friction to manage finances and automate to optimize their financial journey, especially through a troubled economic situation.

The more users and assets it can account for, the more data points for clustering, filtering, and trend analysis using Intuit’s algorithms. The North Star Metric(NSM) could be the number of assets/debts added to the platform. Intuit’s Mint revenue streams are predominately from ads and a small percentage from premium accounts. So logically, this is the metric that predicts the product’s success. Other KPIs and success metrics are listed through the funnel in the GTM strategy section of the blog.

The biggest risk to this feature is to evaluate and assign market value to assets, building APIs for a wide variety of asset classes for the dynamic account reads. But even with the risks involved, when executed strategically and incrementally launched to segmented profiles, the algorithms can be tuned for optimizations, personalization, ranking, and search. This scalable feature is indeed a great value add to the user addressing a major pain point and mutually helping Intuit to differentiate its UVP.

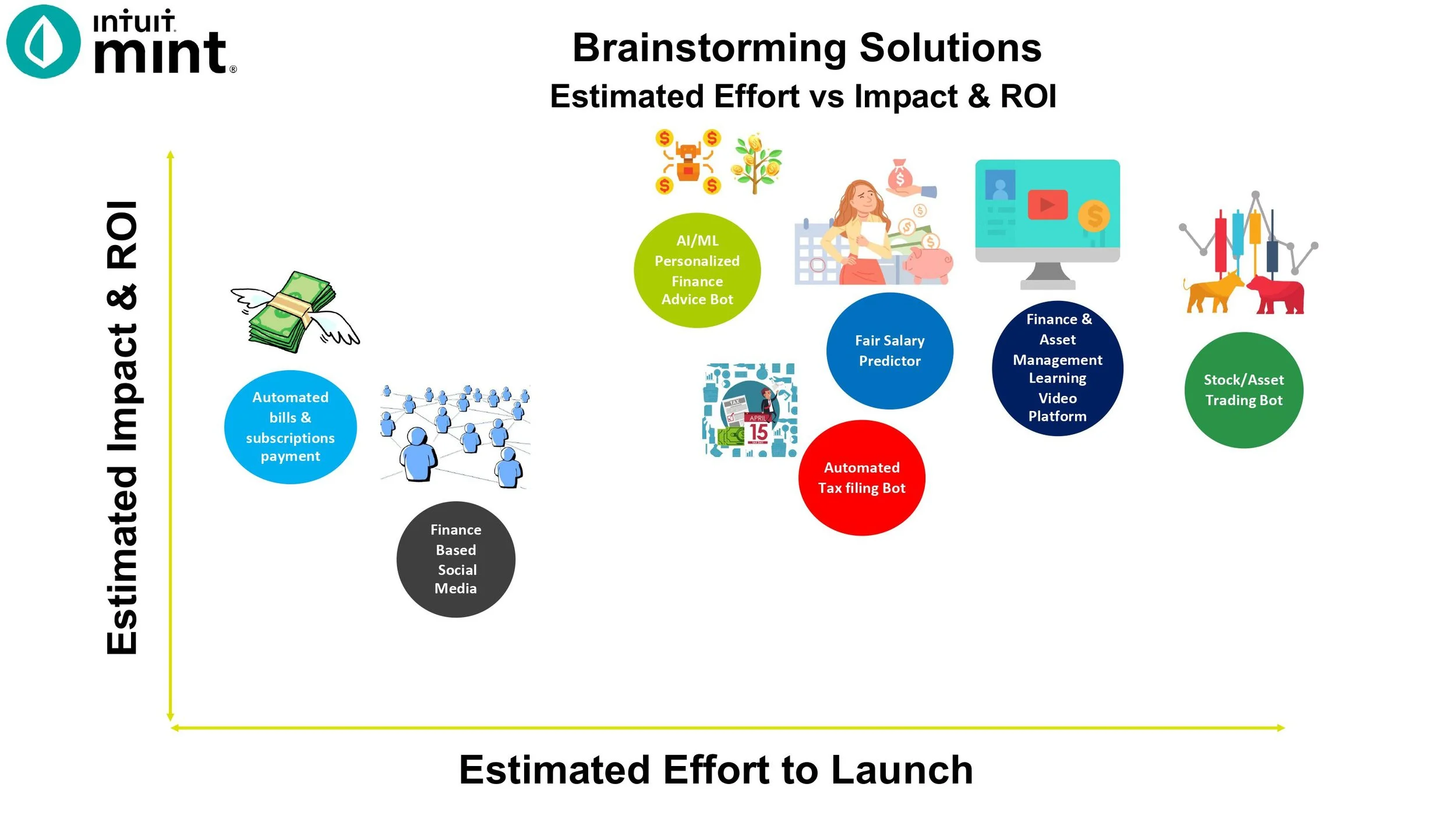

Image 9: Effort vs Impact & ROI estimation

Image 10: Key Performance Indicators(KPI’s) through every stage - Ads Subscriptions Plan

Image 11: User Journey Map for Mint Money Tree Feature

7. Minimum Viable Product(MVP), A/B testing for Product Market Fit

Building the MVP starts with creating custom APIs for all asset classes. Currently Mint has this feature for a few select bank accounts and investment accounts. Expanding this to cover all tangible and intangible asset classes and determining the market value of each asset class (either user assigned or automated) is the first challenge. Something which needs attention is defining a clear data governance policy around holding and sharing users asset’s information diligently, since the platform’s revenue is mostly ad’s based, what data to share is paramount.

For the system design and algorithms, defining the data ingestion, storage, processing, and processing orchestration is critical for periodic data pulls from the database or a scheduler that does that automatically. For the MVP, starting with supervised models gives us clarity and confidence over the data. Over time moving to a hybrid model with either ensemble, layered or AutoML pre-trained models helps in better predictions. Additionally having a basic analytics dashboard help to differentiate model behavior and performance based on user profiles.

For model optimizations, there is a wide range of A/B testing available with Bayesian A/B testing, Frequentist A/B testing, Muti-Armed Bandit(MAB), and Impact Estimation running tests. Mapping out the pros and cons for each and testing features routinely should gather enough data to fine-tune the strategy with a data-driven approach and a clear hypothesis with a high confidence interval on treatment and control groups to optimize the best models across user profiles.

Image 12: User Journey Map for Mint Money Tree

8.Wireframes & Mockups:

Image 13: Mint Money Tree - Al/ML Data Modelling

Image 14: Mint Money Tree - Schematic Diagram

Image 15: Model View Controller API’s connection

Image 16: Wireframes

Image 17: Net Worth Estimator dashboard with Mint Money Tree messages

Image 18: Net Worth Estimator dashboard with personalized financial analytics

9. Go-To-Market Plan, Product growth & scaling

Go-to-Market(GTM) is basically a step-by-step plan with every detail to successfully launch the product. Having a good GTM strategy helps in identifying the market problem for a refined set of users and delivering personalized value to them by positioning the product as their solution. In the real world defining TAM, SAM, SOM, and ICP numbers are highly critical in determining the market share of the problem. While it does involve referring through a lot of data sources to determine the market size and the portion controllable by the product. For the scope of this case study, I have used justifiable numbers from assumptions and estimations shown below.

Image 19: GTM Statistics

9.1) Revamp the strategic narrative aka manifesto with a clear new value proposition

Launching the feature with a purpose, aka manifesto plays a crucial role in getting the product to the hands of the users. It needs to be catchy, and convey exactly the message the product is solving which the users resonate with vividly. Yes, that’s a lot of things in one, but think of all the eye catchy slogans from great products, the fact that you can recollect so of them shows powerful this step is in connecting with the audience.

Image 20: GTM Strategy

9.2) Identifying the initial customer profiles, average customer value, and ideal customer profiles

While the target persona is fairly well defined, for the product to work with a high engagement rate, it needs to be exposed to the right audience aka ideal customer profile(ICP). Using various data sources to target these user segments helps the product to get traction very rapidly.

9.3) Execution, Sales, Marketing, and Customer Acquisition Costs

Pinning down the exact customer acquisition cost (CAC) with a pricing model to increase premium subscription revenue is key in the long term, additionally allotting a budget to regain lost customers and welcome them back to retry the improved product can help boost engagement.

Image 21: Success Metrics and KPI’s

10. Summary

In this case study, I’ve tried to decipher how Intuit’s Mint can approach the problem of stagnating subscriber growth to increase engagement and be a leader in the PFM world through evolving its UVP with data/AI/ML boosted features. While there isn’t a perfect solution, hedging risks, managing tradeoffs, and finding product-market fit to satisfy customer needs are the most preferable options to release new products.

Out of all the solutions, I could come up with, AI/ML Net worth Estimator and Personalized Finance Bot has bubbled up as the top solution through my framework and analysis. While there could be some anticipated friction with a few user segments with data privacy worries, when addressed well it can be put away, but the idea does have merit and long-term potential when strategically implemented.

Image 22: Mint Money Tree Executive Summary

Outro:

In the long term automated investing will take precedence over manual asset tracking. With the influx of virtual assets, currencies and so many more intangible assets, there’s a big need for dynamic asset tracking and management solutions. Intuit is positioned well for this breakout era and it should focus on the big picture of generating the most value for its users on its platform.

How would you solve Intuit’s problem? What would you do differently? Write to me with your solution, I’d love to hear from you.

Here is the TLDR version in a pitch deck.

Disclaimer: All opinions shared on this blog are solely mine and do not reflect my past, present, or future employers. All information on this site is intended for entertainment purposes only and any data, graphics, and media used from external sources if not self-created will be cited in the references section. All reasonable efforts have been made to ensure the accuracy of all the content in the blog. This website may contain links to third-party websites which are not under the control of this blog and they do not indicate any explicit or implicit endorsement, approval, recommendation, or preferences of those third-party websites or the products and services provided on them. Any use of or access to those third-party websites or their products and services is solely at your own risk.